2017 was a year of hopes that had a mixed record in coming true. In international relations, there were a number of successes including visa-free regime for short-term travels of Ukrainians to the EU, the introduction of free trade area with Canada and the full implementation of the Association Agreement between Ukraine and the EU. Ukraine was able to return to the international capital markets for the first time since 2013.

The Parliament finally approved the healthcare reform law, which means that the reform of primary healthcare starts in 2018. The approval of the Education Law became controversial. It means important changes in the status of education establishments and modernisation of education curriculum, but its provision on language of teaching was heavily criticised by Hungary and Poland. Approved pension reform only partially reflected the obligation of country in the framework of the IMF program as higher requirements of working record were complemented by higher than previously expected increases in pensions.

At the same time, the Government failed to approve the land market reform. Instead, the Parliament extended the moratorium on agricultural land sales for another year. The privatization law and the law on credit registry were not approved. The automatic inspection of e-declarations was not also introduced. The Anti-corruption court was not created The Government also did not increase gas tariffs for population as it was previously planned. As a result, Ukraine did not receive scheduled for 2017 two tranches of IMF loan and the final tranche under the MFA III.

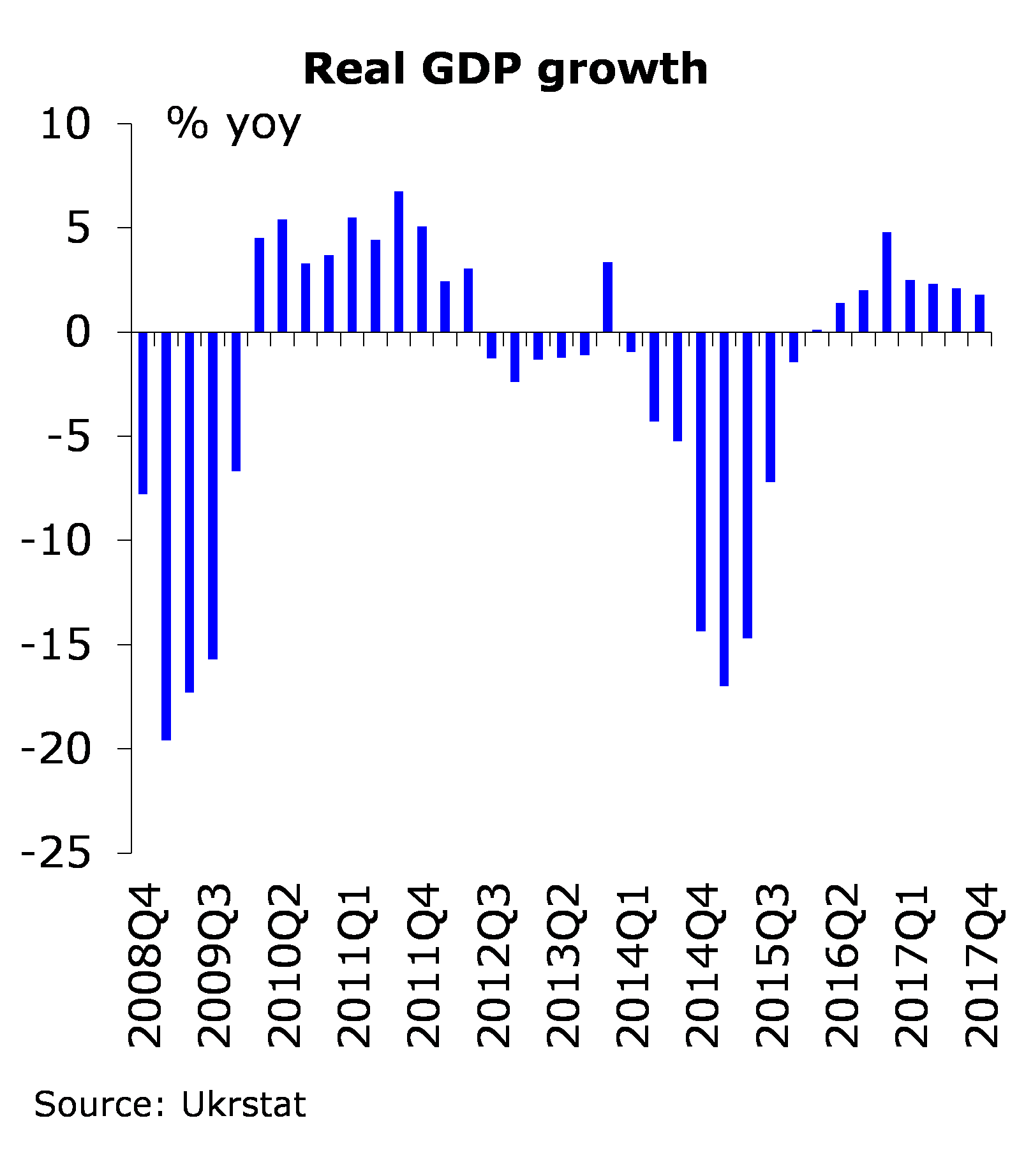

Economic recovery was lower than previously expected: real GDP is estimated to grow at about 2.2% in 2017. Low growth is partially explained by the blocked of trade with the occupied part of Donbas. Inflation was significantly higher than the NBU target due to rapid increase in minimum wage and growth of commodity prices.

Military Conflict in the Eastern Ukraine Remains a Challenge

In 2017, the military conflict with combined Russian-separatist forces in the eastern Ukraine continued in 2017. The most serious escalations of the conflict took place in winter in the town of Avdiivka where the shelling by combined Russian-separatist forces damaged infrastructure and left local residents without water, heating, and electricity in the freezing weather as well as in summer when combined Russian-separatist forces repeatedly broke the temporary ceasefires. With a purpose to counteract Russian disinformation, Ukraine blocked several Russian websites and social media platforms. 203 service members of the Ukrainian Armed Forces were killed in the war in 2017 and 1126 service members were wounded.

Since March 2017, the trade with the uncontrolled eastern parts of the country was stopped as a result of the shipments blocking campaign that was carried out by politicians and activists in protest against trading with Russia-led separatists. Apart from that, in the first days of March, the leaders of the Russia-controlled militant organizations that occupy parts of the Donbas “nationalized” a number of Ukrainian enterprises that operate on the NCA. As the eastern parts of Ukraine supplied the major share of coal to the rest of the country, Ukraine experienced power shortages and had to import coal, while supply chains were disrupted for metallurgical factories in the country that relied on the eastern coal, coke, and ferrous metals. Overall, this negatively impacted the industrial production and Ukrainian exports.

In December, Ukraine was able to make the biggest prisoner exchange since the beginning of the war. Ukraine exchanged 237 imprisoned fighters of illegal armed groups for 74 hostages captured by combined Russian-separatist forces. Earlier in 2017, two members of the Mejlis of the Crimean Tatar people were released from politically motivated imprisonment by Russian occupational authorities in the Autonomous Republic of Crimea, while many more Ukrainian citizens remain captive in the Crimea, in the eastern Ukraine, and in Russia.

Slow Economic Recovery

Real GDP in the first three quarters of 2017 increased by 2.3% yoy due to stronger domestic demand. Gross fixed capital accumulation surged by 19.5% yoy as companies continued to invest in new machinery and equipment and infrastructure after years of underinvestment. At the same time, higher minimum wage and tighter labor market helped spur income growth and domestic demand. However higher domestic demand drove 7.3% yoy growth of imports. Real exports increased by 1.8% yoy as diversification of exports and improved external demand offset the effects of blocked trade with occupied part of Donbas.

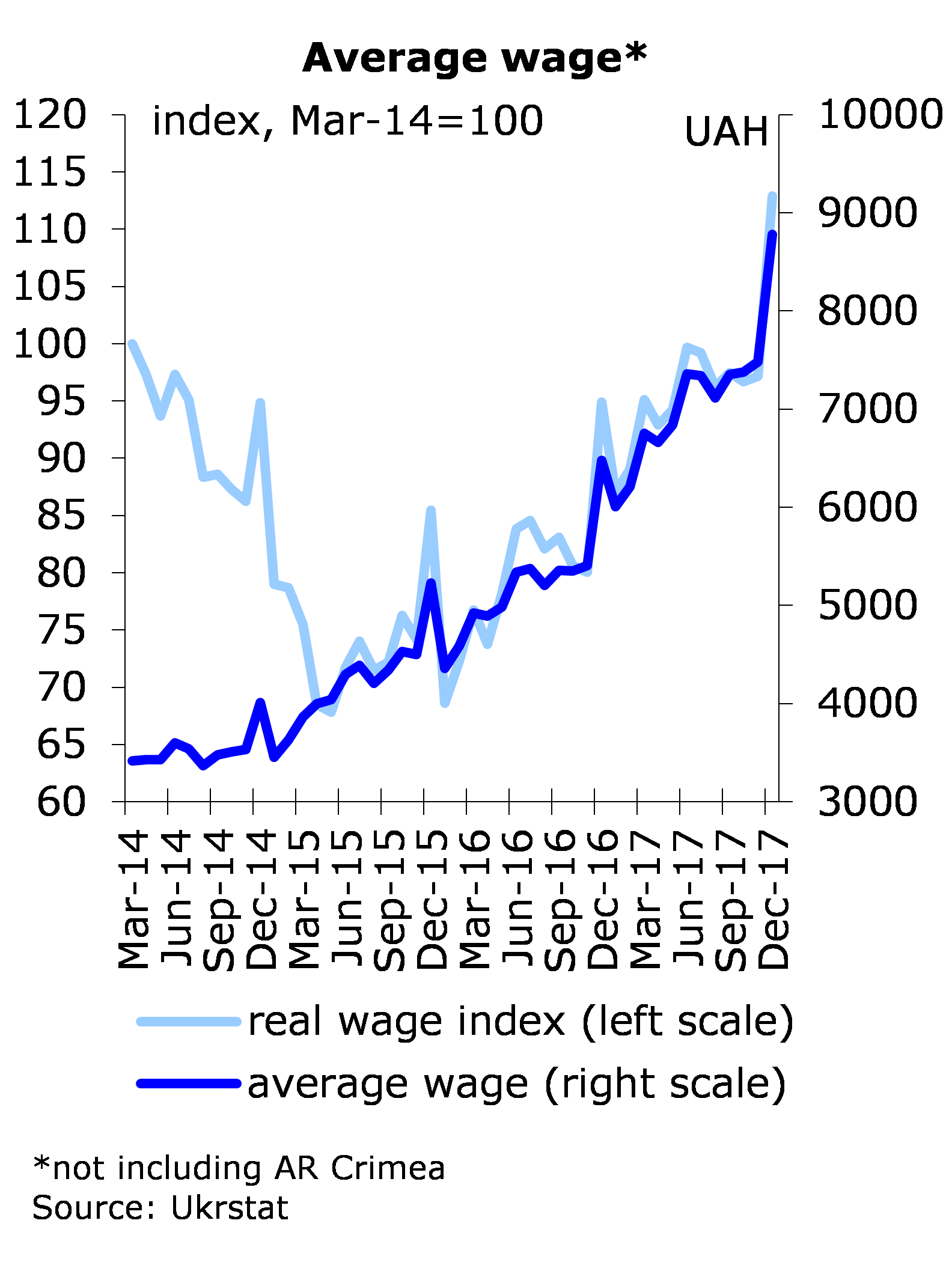

According to the preliminary Ukrstat estimate, the growth of real GDP decelerated slightly to 1.8% yoy in the fourth quarter of 2017. The domestic demand remained the driving force of the growth, while net real exports made a negative contribution to the growth. Real final consumption increased due to higher real disposable income. Overall, wages in 2017 increased by 37.1% in nominal terms and 19.1% in real terms primarily due to hike in minimum wage and improved financial situation of companies. Growth of pensions accelerated in the last quarter of the year due to approved pension reform. Real GDP in entire 2017 is likely to increase by 2.1-2.2%.

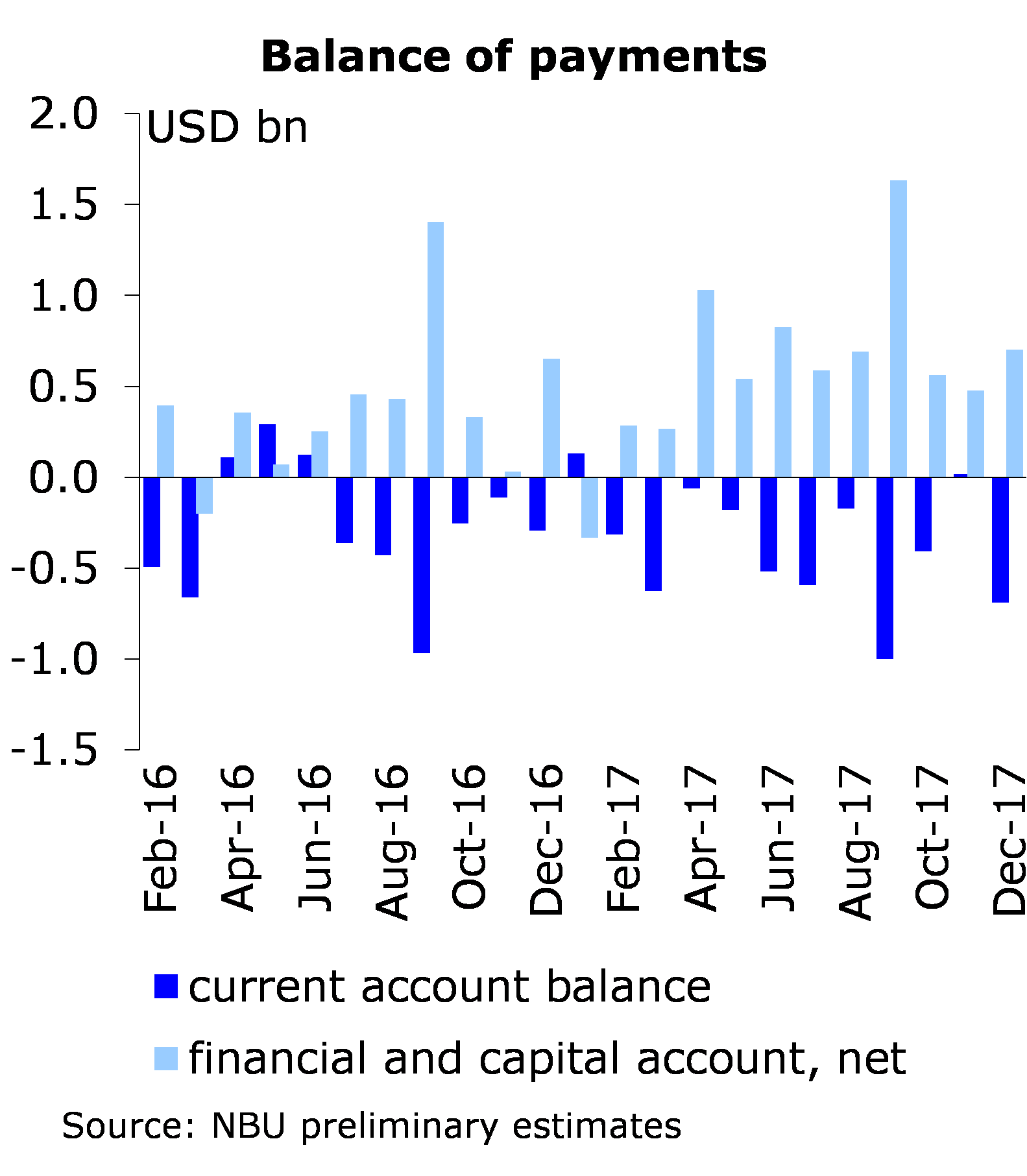

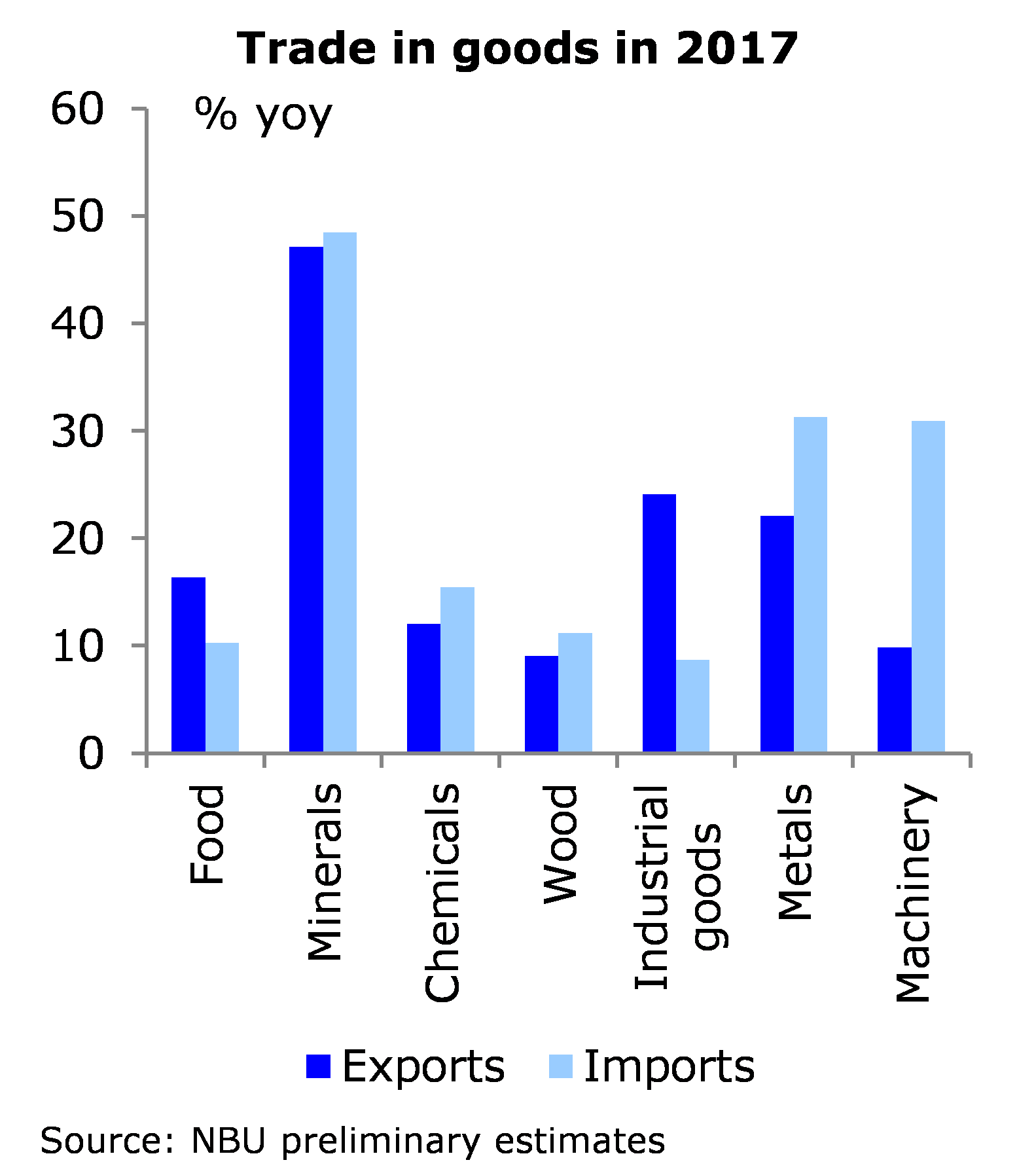

At the same time, real net exports made negative contribution to economic growth in 2017. Exports of goods increased by 18.8% including 31% increase in exports to the EU. This reflected higher commodity prices and likely effects of free trade with EU. Imports of goods increased by 21.1% as mineral imports jumped by 48.5% from low base. Investment demand explained fast growth in machine building imports that increased by over 30.9% and was by 80.5% higher than in 2015. Larger merchandise trade deficit and investment income payments were only partially offset by higher remittance inflows and trade in services surplus. As a result, current account deficit in 2017 reached USD 3.8 bn, which is by 11.2% higher than in 2016. It was fully covered by the financial account surplus that reached USD 6.4 bn (as compared to USD 4.7 bn in 2016). FDI increased to USD 2.3 bn but remained very low. Besides, Ukraine returned to the international capital markets for the first time since 2013. It placed 15-years Eurobonds of USD 3 bn at 7,375% p.a., USD 1.6 bn from which were directed for the buyback purchase of sovereign Eurobonds with maturity in 2019-2020.

Most sectors improved their performance during the year. Industrial output was almost unchanged in 2017 (0.1% decline reported). Growing domestic demand spurred growth of manufacturing output by 4.8%. This offset decline in extractive industry output by 5.7% and electricity production by 6.5% due to blocked trade with occupied part of Donbas. Rising domestic demand also fuelled growth in retail sales and freight volumes. Growing infrastructure investment and commercial property development helped construction to increase by 20.9%.

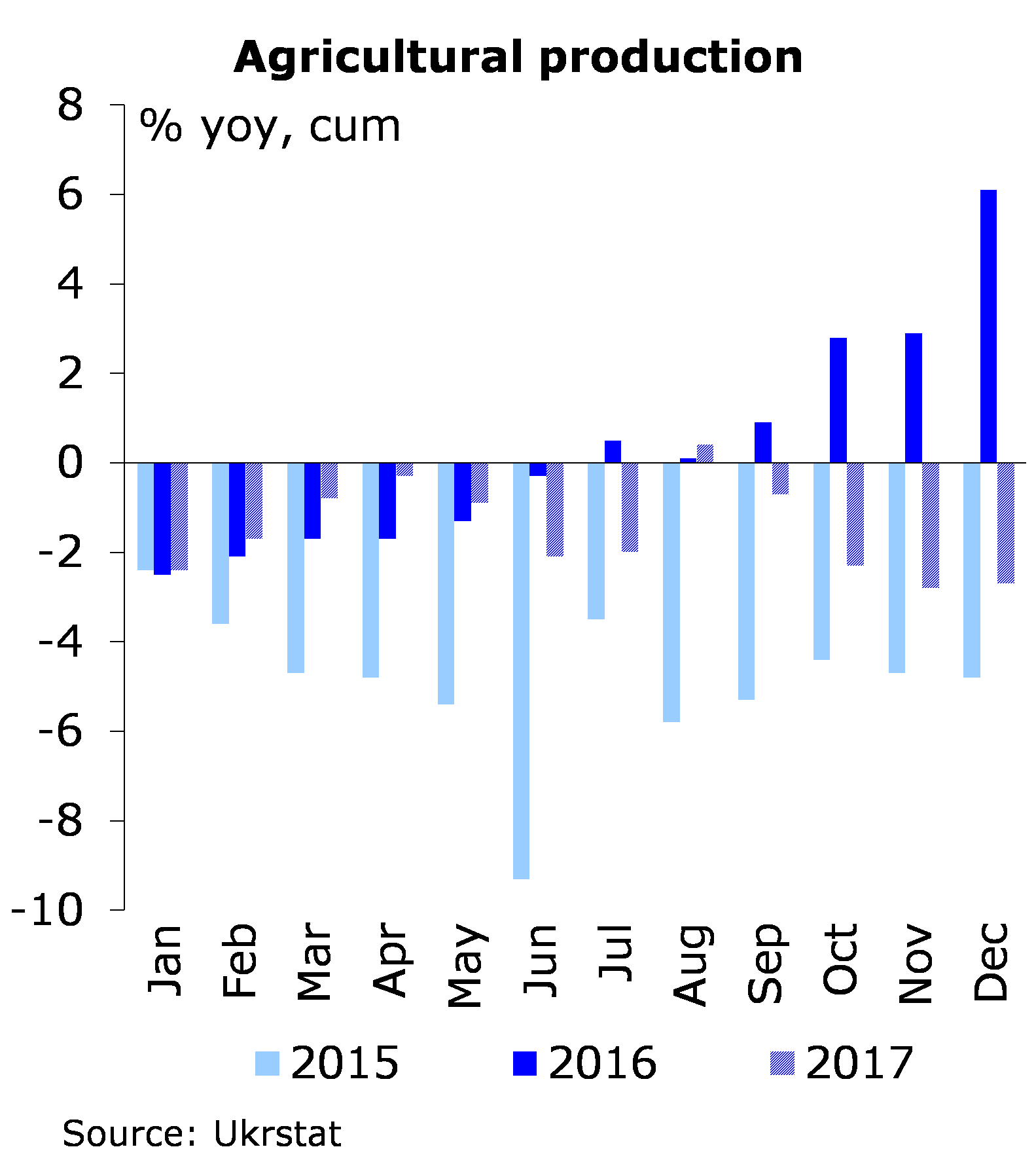

The agricultural production in 2017 declined by 2.7% yoy due to decrease in crop production by 3.6% yoy and livestock production by 0.4% yoy. The production of grains and leguminous crops declined by 7.3% to 61.3 m t likely due to the unfavorable weather during spring. The volume of production of oilseeds increased by 4.4% to 18.3 m t. As of January 1, 2018, the number of cows and pigs decreased by 2.1% yoy and 8.2% yoy, respectively. Still, milk production declined by only 0.5% likely due to higher yields.

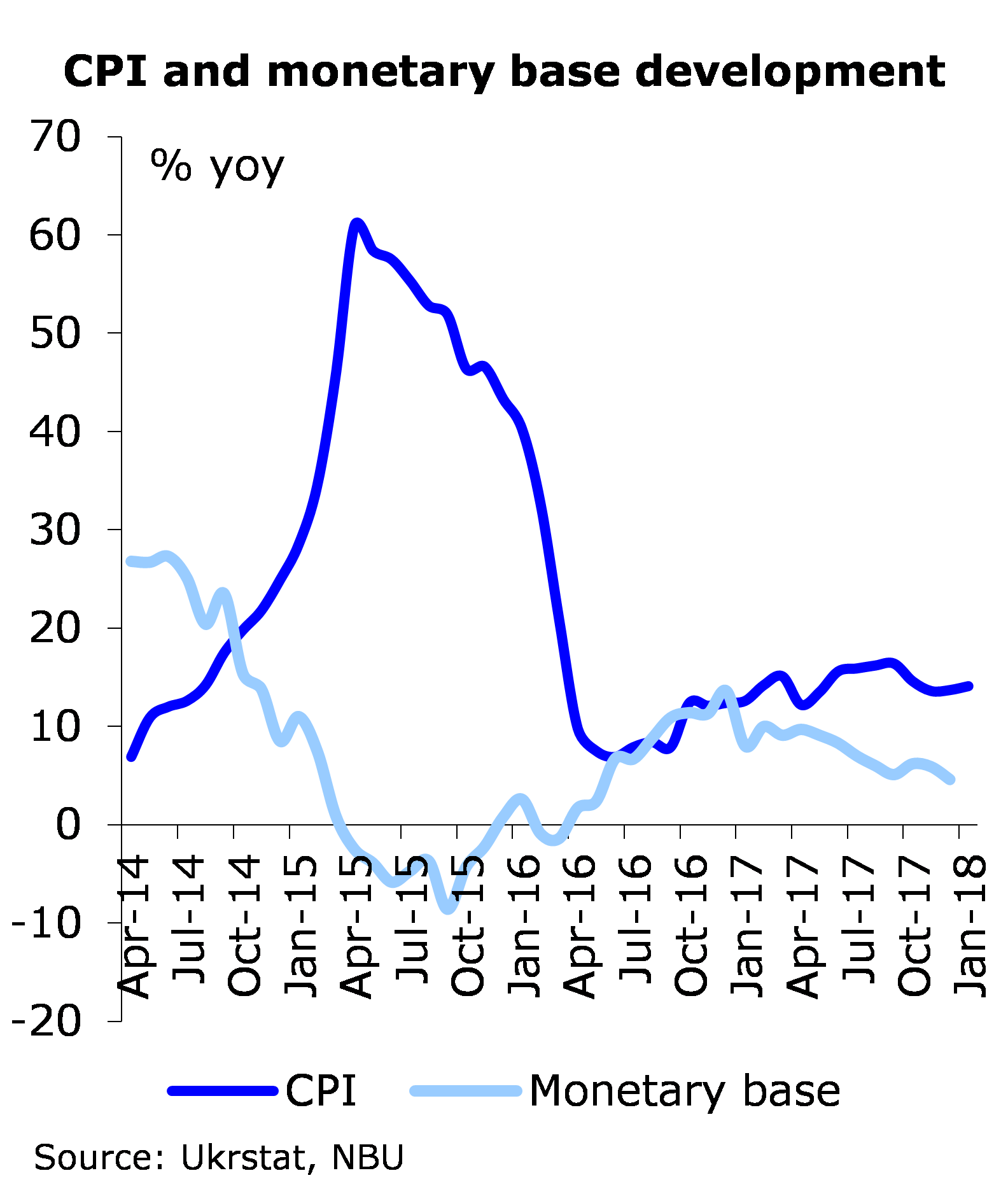

Inflation remained high in 2017 and reached 14.4% on average in 2016 from 13.9% in 2015. This reflected surge in food prices, gradual recovery in consumer demand, and higher labor costs. Food prices increased by 13% while housing and utility costs surged by 27%. In response to higher inflation, the NBU changed policy rate from 14% p.a. to 14.5% p.a. over the year. The NBU reduced the policy rate twice in spring but reverted the changes by the end of the year due to growing inflation pressure. Still, bank interest rates continued falling in 2017. The indicative retail rate for 12-month hryvnia deposits reduced to under 14% p.a. from 18% p.a.

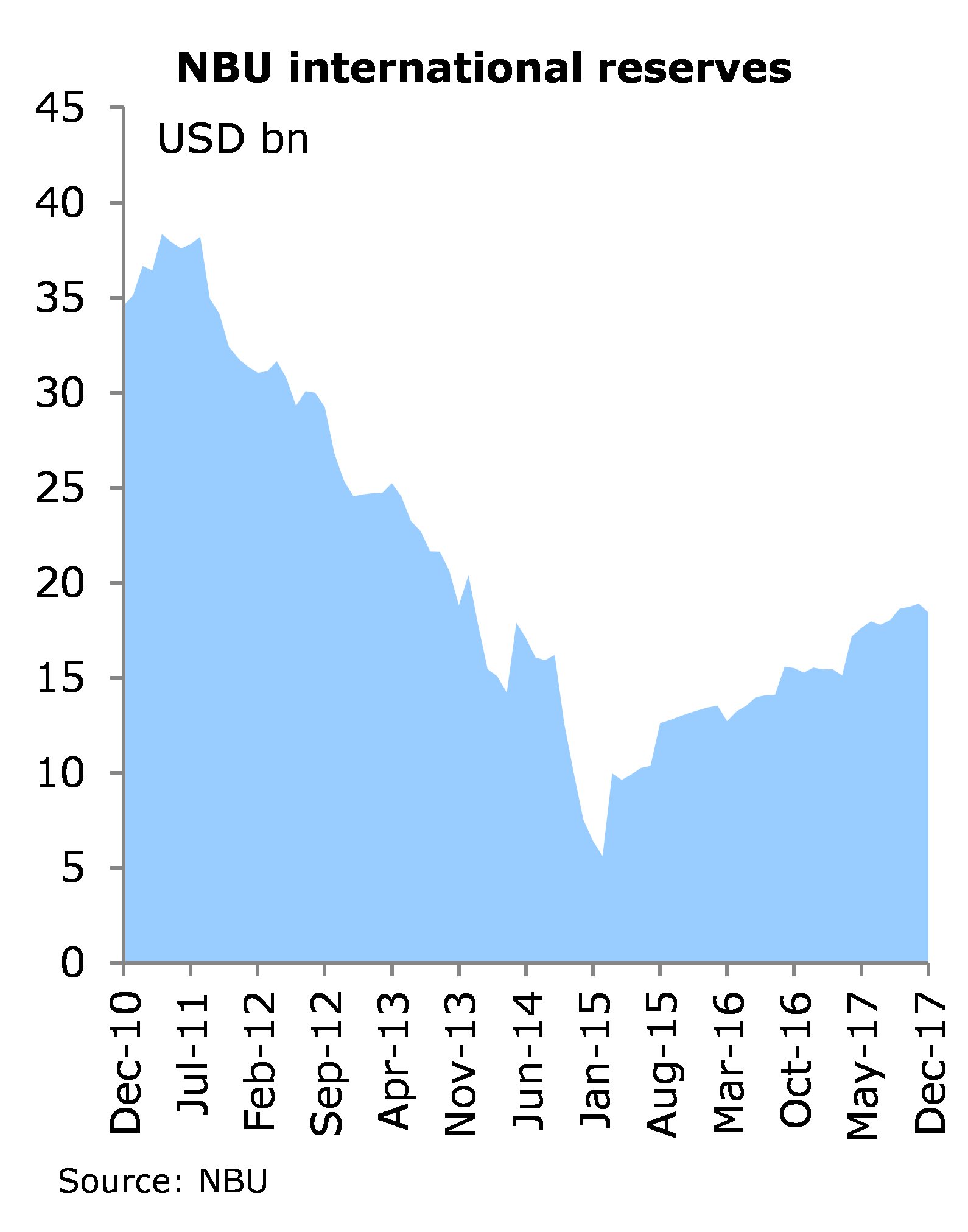

Interbank exchange rate weakened slightly from UAH 27 per USD in the beginning of 2017 to UAH 28 per USD Hryvnia exchange rate followed seasonal pattern where it appreciated in the spring and weakened in the end of the year. Higher consumer and investment demand for imported goods increased pressure on the exchange rate in last quarter of 2017. International reserves reached USD 18.8 bn by the end of 2017 due to public sector foreign currency borrowing and net purchases of foreign currency on the interbank market.

Fiscal Vulnerabilities Remained High

Traditional problems of fiscal policy in the country also repeated in 2017 fiscal year. During the year, central fiscal budget and local budgets were in surplus, which turned into deficit at the end of the year. The traditional one-year fiscal planning again resulted in a peak of fiscal spending in December. Consolidated fiscal expenditures in December accounted for 15.7% of total annual spending. One-third of capital outlays were only financed in the last month of the year. Overall, consolidated fiscal deficit at UAH 42.1 bn was by 2.8 times lower than planned as privatisation plans were again not realised in 2017 (privatization receipts at UAH 3.4 bn accounted for only about 20% of annual target) and borrowings were lower than planned.

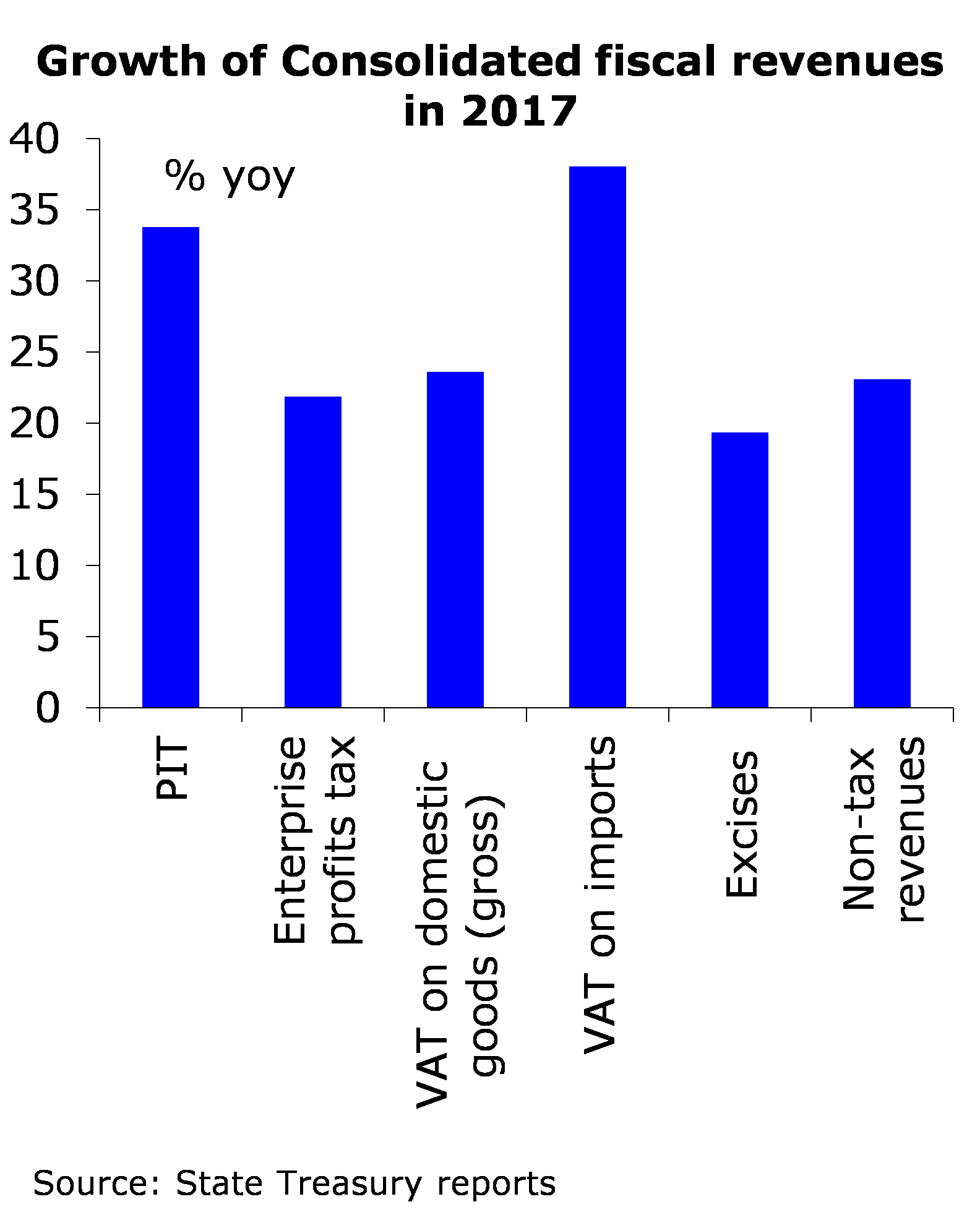

Consolidated fiscal revenues in 2017 for the first time passed trillion-hryvnia mark. They were by 0.7% higher than annual target primarily due to higher than planned VAT revenues. Increased wages, the improved financial situation of companies, and more efficient tax administration resulted in the growth of tax revenues by 27.3%. The growth of non-tax revenues at 23.1% was primarily supported by higher dividends of state-owned companies, larger transfer of the NBU profit, and higher own revenues of budget entities. The Government also received UAH 29.7 bn from special confiscation.

Consolidated fiscal expenditures were by UAH 62.3 bn or by 6.6% lower than planned. As usual, the capital outlays were underfinanced the most (by 22.3% of plan), even though their financing surged in December. Financing of capital expenditures at the end of the year again resulted in low effectiveness and efficiency, which urge the Government to shift to the Medium-Term Expenditure Framework (MTEF) from traditional one-year budgeting. The Government has promised to implement the MTEF starting the Budget 2019.

Still, the Government was able to run primary fiscal surplus, which helped to reduce state debt by 0.5% to UAH 2.1 trillion. However, external fiscal sustainability risks remained high as FX debt accounted for 69.6% as of January 1, 2018. The FX debt to mature in 2018 and 2019 is substantial, which would require the Government to increase fiscal consolidation efforts in 2018.

Some Reforms, But Not Enough

One of the brightest even of 2017 for citizens of Ukraine holding biometric passports was their right for short-term visa-free travel to the EU following the respective approval of the EU Council. The official dialogue between Ukraine and the EU on visa liberalization began in 2008, and in 2010. The EU provided a visa liberalization plan for Ukraine that included a list of measures, such as introducing biometric passports, establishing anti-corruption agencies, and launching electronic assets disclosure system for public officials. However, the EU reserves the right to cancel the visa-free travel for Ukraine if the country does not meet the necessary conditions, in particular, fails to ensure the independence, effectiveness, and sustainability of the anti-corruption institutions.

In the field of cooperation with international partners, the positive step was the Canada-Ukraine Free Trade Agreement (CUFTA), which came into force on August 1, 2017. The Association Agreement between Ukraine and the EU fully entered into force on September 1, 2017. Besides, the EU adopted additional tariff quotas for duty-free importation of a number of Ukrainian agricultural products (cereals, honey, processed tomatoes, grape and apple juices).

In 2017, Ukraine made progress in several essential reforms, which were the most expected by Ukrainian population. In particular, the essential laws were approved for the reforms of healthcare, public administration, secondary education, justice and pension systems. Ukraine also continued the transformation of state-controlled TV and radio broadcasting companies into politically independent public broadcasters by launching the new Ukrainian public broadcaster National Public TV and Radio Company of Ukraine (NPTRCU).

The launch of the healthcare reform was among the most essential steps in 2017 as healthcare remained the least reformed area in Ukraine. The Parliament approved the laws that reorganize health care facilities from budget entities into state-owned and municipal non-profit enterprises and allowing patients to choose their primary care doctor. The financing principles will finally be changed from financing existing infrastructure to payment of provided healthcare. The first steps of the reforms are already planned for 2018.

Justice system reform in 2017 included steps on introducing more transparency into selection of judges, launching a new Supreme Court, and reorganization of the first instance courts. However, the results of the reform are still rather controversial. In particular, in November, President Petro Poroshenko appointed 113 judges of the Supreme Court of Ukraine, even though 25 of them were vetoed by the Public Integrity Council, a civil society group that participated in the selection process. It happed as the High Council of Justice, the state body that nominates judges to be appointed by the President, overrode these vetoes. Overall, the elements of the justice system reform, approved in 2016 and 2017, were insufficient to ensure the fair justice system.

The business climate improved last year due to the continued deregulation measures. To lower administrative pressure on business and promote competition, Ukraine cancelled the government regulation of prices of a number of goods and services, in particular on food products that are considered socially significant. The essential step for the improvement of business climate was the introduction of the automatic VAT refund on the basis of electronic registry, which is available online. According to the State Fiscal Service, between April and October VAT refund arrears were almost eliminated.

High fees in Ukrainian sea ports have long been an obstacle to the development of sea industry in Ukraine. The Cabinet of Ministers decided to increase the ports’ competitiveness by decreasing sea port (ship, channel, lighthouse, sanitary, anchor, private, and administrative) fees by 20% starting 2018.

At the same time, the anti-corruption policy was among the most debated issues over entire 2017. During the year, several Ukrainian anti-corruption activists were attacked and charged with crimes. Additionally, a newly introduced legislation required anti-corruption activists to declare their personal assets starting from 2018, while a number of NGOs and commercial firms reported being searched by law enforcement bodies. At the same time, the anti-corruption institutions continued working with the different levels of success. The National Anti-Corruption Bureau (NABU) indicted several high-ranking officials, including the Head of State Fiscal Service, in the corruption. Several members of the Parliament were stripped of their parliamentary immunity, which opens the possibility to open court trials against them. At the same time, the National Agency on Corruption Prevention (NAPS) has delayed the inspection of e-declarations; the selection of e-declarations for inspection was based on manual approach and not on risk profiling.

As in 2016, the Government again was not able to ensure smooth cooperation with international donors. In particular, Ukraine received only USD 1 bn under the EFF program of the IMF and EUR 0.6 bn under the MFA III from 2017, while lost chances to receive several more tranches of loan from the IMF and the last third tranche under the MFA III. The country did not implement a number of significant reforms including elimination of the moratorium on the sales of agricultural land, establishment of the Anti-Corruption court, and introduction of the automatic inspection of e-declarations of government officials.

Some Progress in Energy Reforms and First Wins in Stockholm

At the end of 2017, the Stockholm Arbitrage Court adopted a final decision in the Naftogaz-Gazprom gas supply case. The court cancelled the “take or pay” clause of the gas contract for 2012-2017, thus, saving the Naftogaz USD 56 bn. It also decreased tenfold the required amount of gas purchase in 2018-2019 and obliged Gazprom to decrease the contracted gas price to market levels. However, the Naftogaz still has to pay the Gazprom USD 2 bn for the gas consumed in 2014. In February 2018, the Arbitrage Court ruling on the gas transit contract obliged Gazprom to pay the Naftogaz USD 4.6 bn for the violation of the “take or pay” clause so overall the Naftogaz won USD 2.6 bn.

Ukraine introduced a new energy market model in accordance with the Third Energy Package with the law “On the Electricity Market of Ukraine”, including the unbundling of transmission and distribution system operator requirements. As required by law, the Energorynok, the national operator of the wholesale electricity market in Ukraine, created a branch ‘Market Operator’ for selling the electricity on the “day ahead” and 24-hour electricity markets according to the new energy market model. In addition, the state enterprise Ukrenergo, the national operator of the electricity network, was transformed into a private joint stock company with a 100% public ownership.

During 2017, Ukraine adopted several other important laws, including the law on general rules for commercial metering of utility services, the law on the Energy Efficiency Fund, and the law on energy performance of buildings. The requirement on energy efficiency certification for several key building categories, including new buildings, is expected to launch a fundamentally new market for the thermal and energy modernization of the buildings in Ukraine. Newly launched Energy Efficiency Fund will partially compensate costs for improved energy efficiency of the buildings. The Fund’s activities are to be financed at the expense of central budget and international donors’ contributions. The State Budget Law for 2018 allocates UAH 1.2 bn for the Fund’s financing, which is unlikely to be sufficient for the effective Fund’s activity.

Ukrainian electricity system operator Ukrenergo signed an agreement on the unification of the electrical system of Ukraine and Moldova with the electricity system of continental Europe ENTSO-E. Synchronization with ENTSO-E requires not only resolving complex technical issues but also introducing different principles of selling electricity (when any consumer in Ukraine can buy electricity from any European producer and Ukrainian producers can export electricity to any consumer in Europe).

At the same time, the Government changed its plans to increase gas tariffs for the population requiring that the Naftogaz should provide the gas to households at the same price as before. This returns price distortions on the Ukrainian gas market and might result in further deterioration of gas infrastructure and overconsumption of gas by the population.

Conclusions

To sum up, there were wins and failures in 2017. The Ukrainian Government was able to approve important reforms, which was still not sufficient to receive scheduled assistance from the IMF and the EU. The year 2018 will be tough as Ukraine should make large progress in many areas, while the elections are approaching in 2019. Among other measures, the country should finally start privatization, establish the Anti-Corruption Court, approve the model of the agricultural land market, and increase gas tariffs for the population.