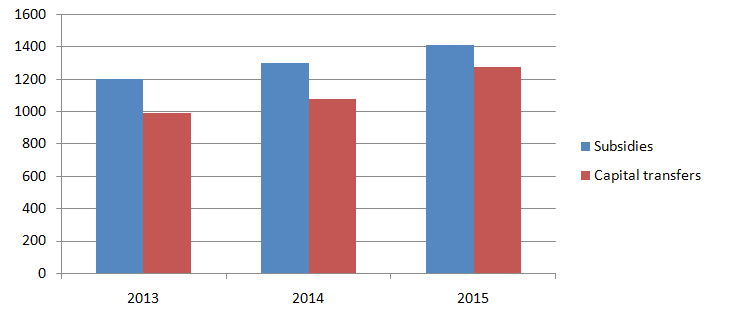

State-owned enterprises (SOEs) are a very important part of the Bulgarian economy. Their revenue in 2015 equals 13% of GDP, but even that number underestimates their economic impact. Key sectors such as energy, railway transport and water supply are dominated precisely by such enterprises. And although on paper SOEs are not part of the state budget, their financial situation has serious impact on public finances. In 2015, the total amount of subsidies and capital transfers from the state budget to public enterprises is BGN 2.7 billion (or 3.1% of GDP), and they have remained relatively stable around 3% of GDP in recent years.

Figure 1: Subsidies and capital transfers from the state budget to public enterprises (mln BGN) 2013-2015

Source: Ministry of Finance in Bulgaria

Source: Ministry of Finance in Bulgaria

Despite their importance for the economy and the burden on the budget, no analysis on the financial position of the enterprises in the public sector has yet been published. This is a serious problem, especially given the fact that in recent years the process of privatization of these enterprises is practically frozen, while subsidies and capital transfers to them continue to grow even faster than GDP.

This led IME to examine the financial position of the public enterprises, trying also to conduct a financial analysis based on some of the most common secondary indicators of return and indebtedness. For this purpose, we have consolidated the data from the financial statements of all public enterprises (158 in total) for which the Ministry of Finance has published reports on each of the last three reporting years (2013, 2014 and 2015).

The analysis focuses on three main indicators, by which we can gain a relatively complete picture of the financial health of the companies in the public sector. These indicators are:

1) net profit after tax;

2) annual return on assets;

3) the size and dynamics of indebtedness expressed by the ratio of liabilities to equity.

Data show that in general the financial position of the state-owned enterprises deteriorated in 2014 and 2015 compared to the base year 2013. The number of loss-making enterprises increased significantly to 72 in 2014, and although it dropped to 62 in 2015, it remains above the level of 55 back in 2013. The overall financial result deteriorated significantly – from a BGN 493 mln net profit in 2013 to a BGN 266 mln loss in 2014. In 2015, the situation once again improved and a net profit was reported (BGN 85 mln). The liabilities of the enterprises grow in each of the reviewed years – in 2014, the pace of debt accumulation outpaced GDP growth.

The median return on assets is very low. In each of the reviewed years it is not even approaching 1%, which means that a large part of the SOEs practically do no account any returns. For comparison, in the private sector the recommended return that a company must reach to be considered as a good investment amounts to approximately 5%.

The level of indebtedness has in general fallen during the period, but has risen in certain key sectors – such as health and energy. It is worrying that the median ratio of debt to equity for enterprises with annual revenues above BGN 100 mln is six times higher than the median for all enterprises. This clearly shows that the largest and most important companies are also most indebted.

If we focus on the 10 state-owned enterprises with the highest revenues (which form 78% of the revenues of all SEOs), we will notice that their financial result is significantly worse than the average. Their average revenue is lower than that of all public companies in each of the reviewed years. The same goes for the return on their assets. In 2014 and 2015, the median return on assets of the 10 largest SOEs is negative. Five of these enterprises actually lost money in 2015, compared to three in 2013. As a result of this poor economic performance, their median ratio of debt to equity rapidly rose from 0.83 in 2013 to 1.33 in 2015, which is an increase of over 60%.

It must also be noted that recently some SOEs have improved their financial situation “on paper” through accounting tricks. For example, the level of indebtedness of BDZ–Passenger Services significantly declined in 2015 due to accounting entries. As of December 31, 2015, the value of the company’s equity is over 90% higher compared to a year earlier. However, this is mainly due to revaluation of certain fixed assets rather than debt repayment.

In the first half of 2016, there was a similar improvement in the net profit of BDZ Freight Transport, which was mainly the result of lower reported depreciation due to change in accounting policy. Such purely accounting improvements do not imply an actual optimization activities of the SOE concerned.

The data show that the financial position of SOEs as a whole has remained bad in recent years – profits are falling, returns are low or even negative in the top ten enterprises. The indebtedness of major players is growing rapidly. Along with the deterioration, however, subsidies and transfers from the state budget to these companies have continued to grow, despite a chronic budget deficit. Furthermore, in recent years the process of privatization is not only frozen, but even is going in the opposite direction – already privatized companies are re-nationalized, while others are added to the restrictions list for privatization. It is high time for the government policy on public enterprises to be revisited by clearing the restrictions list and privatization of the majority of SOEs.