For another year in a row, Poland ranks near the bottom among OECD countries in the International Tax Competitiveness Index published annually by the Tax Foundation (35th out of 38 countries). The International Tax Competitiveness Index shows to what extent the solutions used in OECD countries are consistent with the principle of tax neutrality and remain competitive relative to other countries.

The index assesses key areas of the tax system: taxation of personal income together with social security contributions, taxation of corporate income, taxation of consumption, property taxation, and taxation of international activity. Poland’s low overall position is driven in particular by the poor assessment of consumption taxes (VAT), wchich neutrality is undermined by numerous exemptions and reduced rates. The score is also dragged down by the treatment of cross-border transactions and by property taxation, which inefficiently burdens the holding and transfer of certain types of assets.

The assessment of income taxes is mixed. On the one hand, Poland’s top marginal tax rates are in many situations lower than, or close to the OECD average. On the other hand, the Tax Foundation points to many elements that fall short of the postulates of simplicity and neutrality of the tax system.

The analysis suggests that, to make the Polish tax system more supportive to economic growth, Poland should in particular broaden the VAT base and reform the market-distorting and fiscally inefficient property taxation. It would also be beneficial from the perspective of economic development to expand the ability to offset tax losses over time and to accelerate tax depreciation allowances.

The shape of the tax system is one of the most important factors determining the strength of an economy. A well-designed tax system means that tax rules are simple to apply, support economic development, and at the same time provide the state with sufficient revenues to carry out its tasks. By contrast, a poorly designed tax system generates costs for taxpayers and the tax administration, distorts economic decisions, and slows economic growth.

OECD countries use different tax solutions. To compare tax systems, the Tax Foundation publishes the International Tax Competitiveness Index each year. The index promotes simplicity, neutrality, transparency, and stability as key principles of a well-designed tax policy. It aims to show to what extent tax systems in OECD countries support economic growth. The ranking reflects how closely solutions applied in each country follow the principle of tax neutrality and how competitive they are relative to other countries. The index assesses solutions in the following areas: taxation of personal income (PIT) together with social security contributions, taxation of corporate income (CIT), taxation of consumption (for most countries, including Poland, VAT), property taxation, and taxation of international activity. The Tax Foundation’s ranking focuses primarily on the design of tax rules, while the amount of revenue raised is secondary. This is based on the view that a given level of tax revenue can be achieved through different tax designs; the key is to raise it through a well-designed system that is beneficial to growth. Tax policy is one of the key factors influencing investment and development.

For another year in a row, Poland ranks low in the International Tax Competitiveness Index. In the latest edition, Poland’s tax system placed 35th out of 38 OECD countries, a drop of six positions compared to the previous year. This is particularly alarming given rising spending needs, for example on transfer payments, defense, and health care-combined with the need to maintain investment at a level that supports strong economic growth.

Poland’s low ranking reflects the use of overly complex tax solutions, which generate high compliance and administrative costs. The score is reduced by tax rules that distort the decisions of households and entrepreneurs and thereby limit activity and economic growth. Poland’s distant position in the ranking is driven in particular by weak performance in personal income taxes and social contributions1, consumption taxes, property taxes, and international taxation (35th, 35th, 28th, and 31st place respectively out of 38 countries).

Corporate income taxation also fails to fully meet the postulates of competitiveness and neutrality; however, relative to other countries Poland performs somewhat better here and ranks 14th. The best performers in this year’s edition are Estonia, Latvia, and New Zealand, while Colombia, Italy, and France rank lowest.

Methodology of the Ranking

The International Tax Competitiveness Index assesses five key areas of the tax system: personal income taxes, corporate income taxes, consumption taxes, property taxes, and taxes on international activity. Each area is divided into subcategories, which are in turn described by a set of features (variables). In total, the ranking uses 42 variables. For example, the corporate income tax area is divided into three subcategories covering the tax rate, cost recovery over time, and tax preferences/complexity; each is described by a number of detailed variables. In turn, the consumption tax area is divided into two subcategories: the tax rate and the tax base. The latter is described by variables such as the revenue threshold for VAT registration exemptions and the VAT base as a share of total consumption.

The ranking measures the relative position of each country’s tax system within the OECD group. The country with the best position receives 100 points. This does not mean it has a perfect tax system, but that it performs best within the OECD. The ranking focuses on neutrality and competitiveness. Therefore, it does not measure the overall tax burden relative to GDP, nor the fiscal efficiency of individual taxes. The underlying assumption is that a given level of tax revenue can be achieved through different tax designs; the key is to achieve it through a well-designed system that is pro-growth.

Poland’s Position in the Ranking

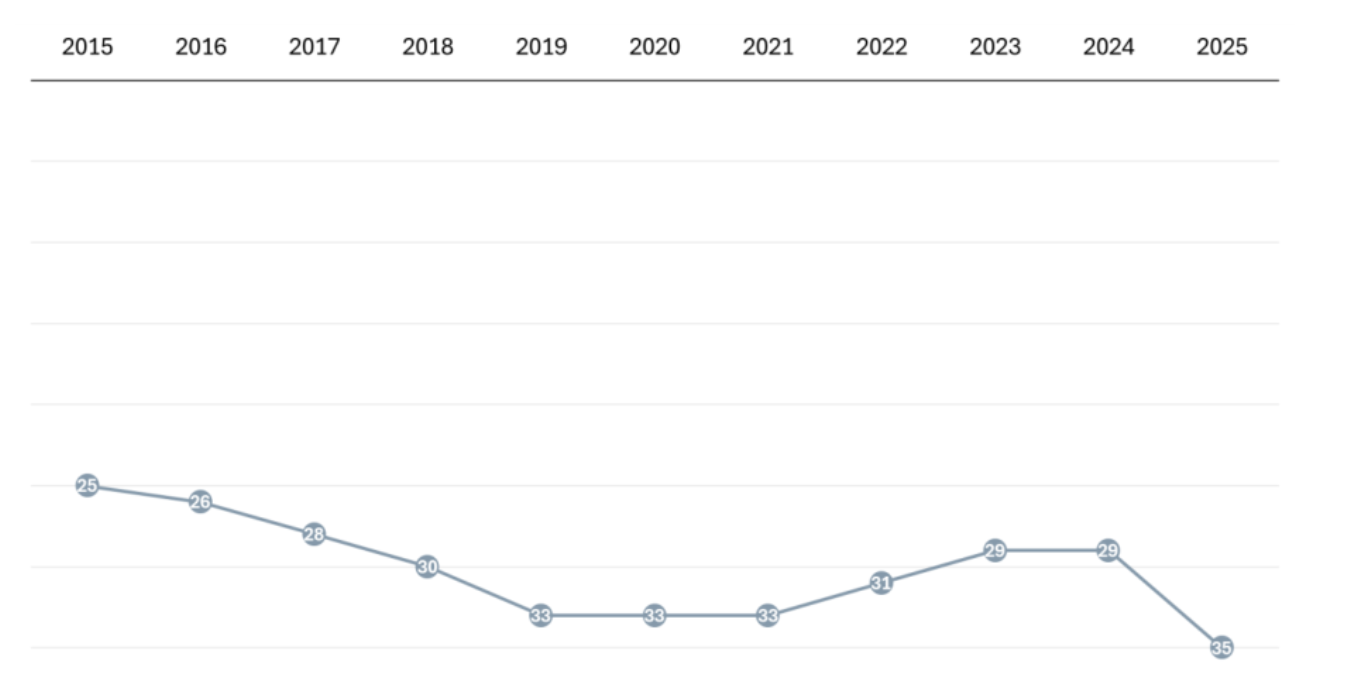

For many years, Poland has ranked low in the International Tax Competitiveness Index. In the latest edition, Poland placed 35th out of 38 OECD countries, a drop of six positions compared to the previous year. As shown in Figure 1, the highest position Poland achieved over the last decade was 25th – ten years ago. Even then, it was difficult to consider the system to be competitive and neutral. Today the situation is much worse. This reflects both changes in Poland that are unfavorable from the perspective of neutrality and competitiveness and a relative improvement in other countries.

Figure 1: Poland’s position in the International Tax Competitiveness Index over the last decade.

Source: Tax Foundation

Source: Tax Foundation

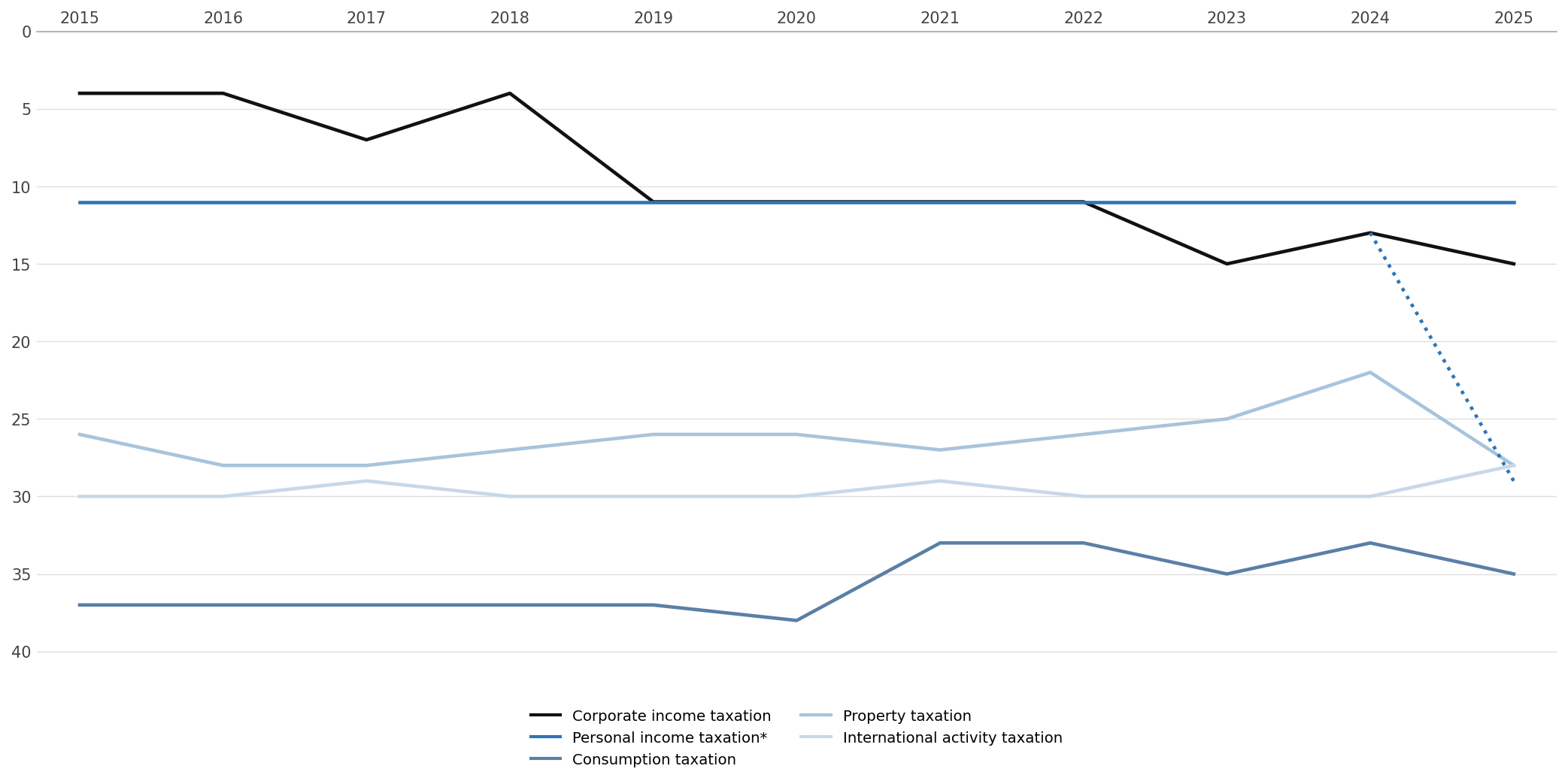

Figure 2: Poland’s position in selected areas of the tax system over the last decade.

Source: Tax Foundation

The weakest area is consumption taxation (currently 35th out of 38 countries). This is mainly due to the low share of the VAT tax base in total consumption (46%). This results from carve-outs in the VAT design, such as exemptions and reduced rates. The Tax Foundation also notes that Poland’s revenue threshold that allows businesses to apply the VAT exemption is relatively high. It currently amounts to PLN 200,000, roughly 1.5 times the average threshold in OECD countries.

International taxation is rated slightly better, mainly due to Poland’s relatively large number of double taxation treaties and the scope of the dividend exemption. However, compared to the previous edition of the report Poland’s position deteriorated from 22nd to 31st. This is the result of introducing top-up taxation rules (the GloBE minimum tax).

Poland’s position in property taxation has been relatively stable over the last decade (currently 28th). The Tax Foundation points to numerous taxes imposed both on holding wealth and on transferring it, including certain elements of the civil law transactions tax that resemble a financial transaction tax. Moreover, property taxes should be rationalized because, to a large extent, they do not reflect market values of assets, increase the cost of capital and distort economic decisions, while at the same time they do not contribute significantly to public revenues.

Against this background, Poland performs relatively better in corporate income taxation (14th place). For understandable reasons, the ranking cannot fully reflect the complexity and intricacy that characterize income taxation in Poland. Nevertheless, Poland’s higher position is driven, among other things, by moderate top marginal tax rates, which reduce the overall cost of doing business that results from an improperly designed tax base. The main weaknesses in CIT include limited possibilities to offset tax losses over time, relatively long depreciation periods for fixed assets, and tax incentives that in practice may amount to subsidising certain types of activity.

Additionally, Poland’s decline in this area from 12th to 14th place was influenced by the introduction of a domestic minimum income tax, which affects low-profit or loss-making companies. It further complicates the CIT system, which already provides, for example, a reduced 9% rate for small taxpayers and the option to choose the so-called Estonian CIT for selected categories of taxpayers.

In general, accelerating tax depreciation of fixed assets is among the most effective tools to support business investment and long-term economic growth, because it reduces the cost of capital and thereby affects the returns on new investments. Similarly, allowing firms to offset tax losses more flexibly over time would reduce the disproportionately high burden on investments with highly volatile income over time. This would be beneficial for start-ups and for increasing spending on research and development.

Table 1: International Tax Competitiveness Index (2025 edition)

| Rank | Country | Total score |

CIT (rank) |

PIT & contrib. (rank) |

Cons. (rank) |

Prop. (rank) |

Intl. (rank) |

| 1 | Estonia | 100.0 | 2 | 2 | 22 | 1 | 7 |

| 2 | Latvia | 92.8 | 1 | 7 | 20 | 7 | 6 |

| 3 | New Zealand |

87.8 | 31 | 6 | 1 | 4 | 22 |

| 4 | Switzerland | 86.0 | 10 | 8 | 2 | 36 | 1 |

| 5 | Lithuania | 81.8 | 3 | 9 | 25 | 10 | 15 |

| 6 | Luxembourg | 81.0 | 20 | 22 | 8 | 16 | 5 |

| 7 | Australia | 79.7 | 29 | 15 | 9 | 2 | 33 |

| 8 | Israel | 78.9 | 11 | 32 | 11 | 5 | 10 |

| 9 | Hungary | 78.7 | 4 | 3 | 38 | 22 | 4 |

| 10 | Czechia | 77.4 | 8 | 10 | 32 | 6 | 11 |

| 11 | Sweden | 76.1 | 6 | 19 | 26 | 8 | 13 |

| 12 | Turkey | 75.9 | 21 | 5 | 17 | 24 | 8 |

| 13 | Canada | 73.9 | 22 | 27 | 7 | 25 | 18 |

| 14 | Slovakia | 73.3 | 24 | 1 | 34 | 9 | 24 |

| 15 | United States |

72.5 | 9 | 17 | 4 | 30 | 35 |

| 16 | Netherlands | 71.4 | 23 | 30 | 14 | 21 | 3 |

| 17 | Costa Rica |

71.4 | 34 | 23 | 6 | 12 | 30 |

| 18 | Mexico | 70.1 | 26 | 14 | 12 | 3 | 36 |

| 19 | Austria | 69.6 | 19 | 26 | 16 | 17 | 16 |

| 20 | Germany | 68.9 | 30 | 33 | 13 | 14 | 9 |

| 21 | Norway | 68.8 | 13 | 29 | 23 | 15 | 14 |

| 22 | Japan | 67.8 | 35 | 34 | 5 | 23 | 25 |

| 23 | Greece | 67.0 | 16 | 4 | 30 | 29 | 23 |

| 24 | Finland | 66.8 | 7 | 28 | 28 | 19 | 19 |

| 25 | Slovenia | 66.8 | 12 | 11 | 29 | 26 | 21 |

| 26 | Korea | 66.3 | 25 | 38 | 3 | 31 | 29 |

| 27 | Denmark | 64.3 | 17 | 36 | 19 | 13 | 34 |

| 28 | Chile | 63.8 | 32 | 24 | 10 | 11 | 38 |

| 29 | Iceland | 63.7 | 15 | 20 | 24 | 27 | 26 |

| 30 | Belgium | 63.2 | 18 | 13 | 27 | 32 | 27 |

| 31 | Ireland | 61.3 | 5 | 37 | 36 | 18 | 28 |

| 32 | United Kingdom |

59.1 | 28 | 25 | 33 | 37 | 2 |

| 33 | Portugal | 58.2 | 36 | 21 | 21 | 20 | 32 |

| 34 | Spain | 57.9 | 33 | 18 | 18 | 35 | 17 |

| 35 | Poland | 54.7 | 14 | 35 | 35 | 28 | 31 |

| 36 | Colombia | 51.1 | 37 | 12 | 15 | 33 | 37 |

| 37 | Italy | 50.3 | 27 | 16 | 37 | 38 | 20 |

| 38 | France | 45.8 | 38 | 31 | 31 | 34 | 12 |

Source: Tax Foundation

Poland’s position in the personal income tax area is influenced, among other factors, by the tax and non-tax costs of labor. The ranking also takes into account the so-called solidarity surcharge, which applies to the highest-income taxpayers whose annual income exceeds nine times the average wage.

For many years, the most competitive tax system in the OECD has been Estonia’s. Its high position is due, among other things, to exempting reinvested profits from tax. In the so-called distributed profits tax, tax is due only when profits are paid out to owners. Latvia ranks second, where an Estonian-style CIT has also been introduced, and New Zealand ranks third. Colombia, Italy, and France rank lowest, due to complex taxes that distort taxpayers’ decisions and high-top marginal tax rates. Table 1 presents the current position of OECD countries in the ranking.

Written by Anna Leszczyłowska – Research Fellow, Tax Foundation, and Assistant professor at the Poznań University of Economics and Business & Alex Mengden – Global Policy Analyst, Tax Foundation