In early August 2025, the Ministry of Climate and Environment presented a draft act on extended producer responsibility (EPR). The draft raises serious concerns. The Ministry claims that the current system “does not deliver satisfactory effectiveness”. Meanwhile, in 2023 Poland’s packaging waste recycling rate was higher than the EU average.

The Ministry draws from the Czech and Hungarian models. The European Commission has indicated that Czech solutions may breach EU competition rules, while the Hungarian system is among the worst in Europe. At the same time, the Ministry ignores the successes of decentralized models. Once again, private competition in a sector is to be replaced by a state monopoly. Such actions have very negative consequences: they increase uncertainty for businesses and discourage investment.

Nationalizing waste management will increase costs for citizens and weaken market incentives. The new EPR system will not improve public finances—it is associated not only with new revenues, but also with new expenditure.

There is an ongoing debate about changes to Poland’s extended producer responsibility (EPR; Polish: ROP) system.1 In principle, EPR is meant to shift the costs and responsibility onto the “polluter”, i.e. packaging producers. The need to reform stems from EU directives aimed at improving waste management.

Poland was originally supposed to introduce these changes in 2023, but has still not done so. In early August, the Ministry of Climate and Environment (MKiŚ) presented an extensive draft act that raises serious concerns.

If the proposed act enters into force, Poland will move towards a centralized and ineffective system. It will be costly and will weaken market incentives to develop innovative and environmentally friendly solutions. What is more, the proposed changes will primarily be borne by consumers, as the Ministry itself notes in the regulatory impact assessment:

“A negative financial impact on citizens can also be expected, due to the potential pass-through of EPR-related burdens imposed on businesses into product prices.”

The Current Waste Management System Is Improving…

Poland’s current system is based on documents confirming the recycling of packaging waste (DPR) and its European supply/export for recycling purposes (EDPR). Companies placing packaging on the market can either manage recycling themselves, transfer responsibility to packaging recovery organizations (OOO), or pay a product fee to the Voivodeship’s Marshal’s Office, which effectively acts as a penalty. In 2024, producers paid PLN 1.4 billion for DPR and EDPR documents.

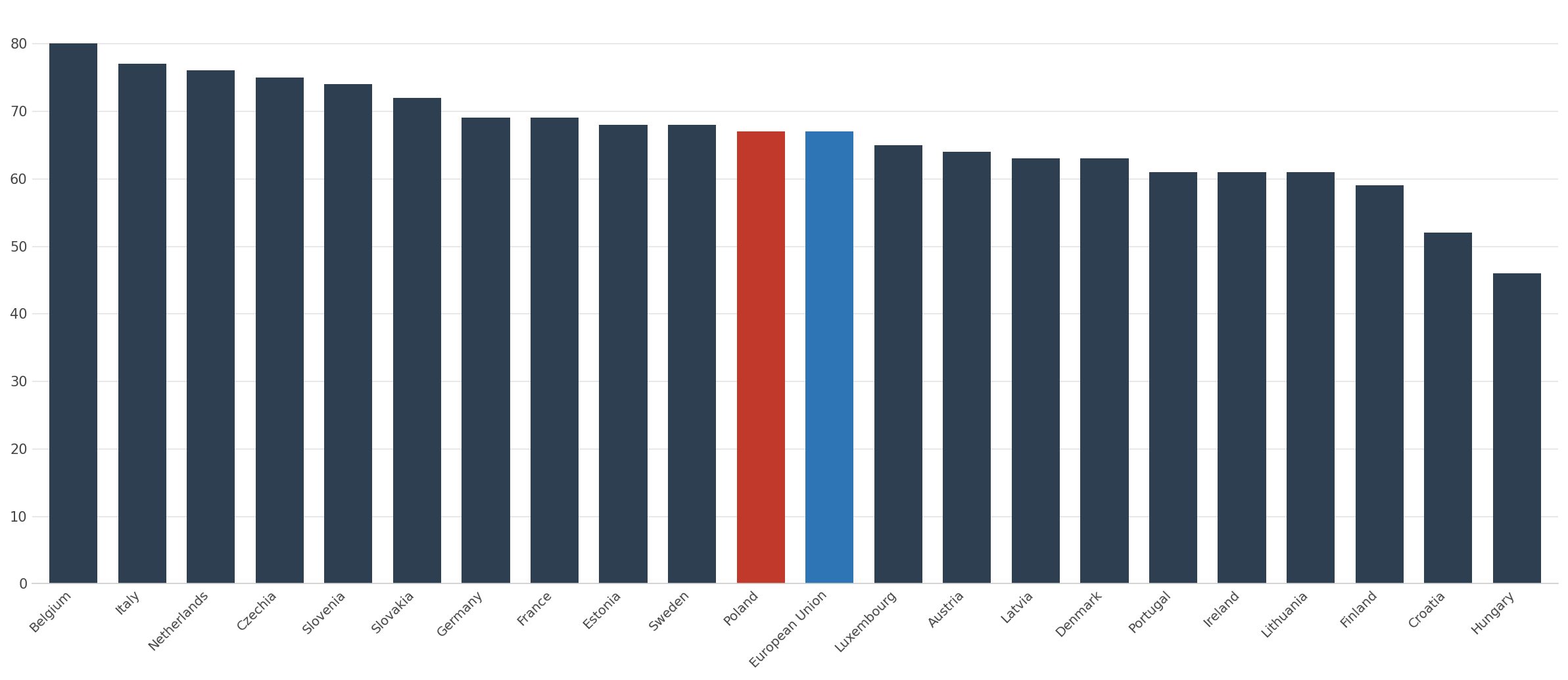

In the regulatory impact assessment, the Ministry claims that the current system “does not deliver satisfactory effectiveness”, without providing data to support this statement. Meanwhile, in 2023 Poland’s packaging waste recycling rate was slightly higher than the EU average (Figure 1). Despite progress, Poland still lags behind Belgium, Italy and the Netherlands, which are among the EU leaders. In a recently published report, the Supreme Audit Office (NIK) pointed to problems in waste management and in implementing EU recommendations, resulting from negative actions by the public administration.7

The current system relies on OOOs, which are set to be liquidated after the reform (although, at the same time, under Article 198 p.3 of the draft they are to act as collectors of the packaging fee). This means that private firms operating on the Polish market for over two decades will be forced to cease operations. This is not the first case in Poland where private competition in a sector is to be replaced by a state monopoly. Such actions by successive governments have very negative consequences: they increase uncertainty for businesses and discourage investment. It is therefore hardly surprising that Poland’s private investment rate is among the lowest in the EU.

Figure 1: Share of packaging waste recycled in 2023 (%)

Source: FOR’s own calculations based on Eurostat data

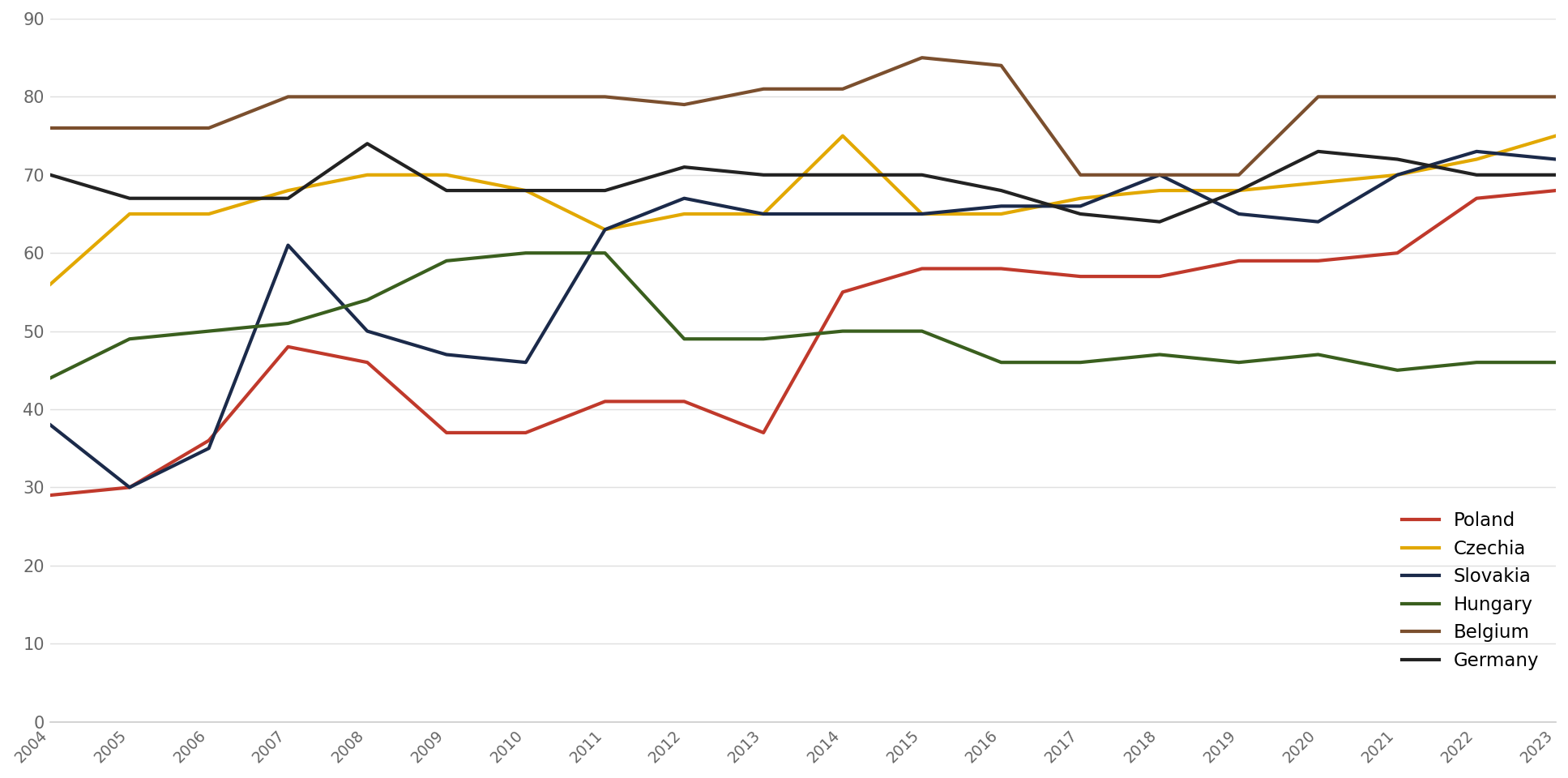

Under the EU Packaging and Packaging Waste Regulation (PPWR), at least 65% of packaging waste should be recycled in 2025, and at least 70% in 2030. Poland therefore needs effective reforms that will support higher packaging recycling. Since the legal changes introduced in 2014, the recycling rate has been gradually increasing, but Poland still lags behind its southern neighbors—Czechia and Slovakia (Figure 2).

Figure 2. Share of packaging waste recycled

Source: FOR’s own calculations based on Eurostat data

…But the Government Is Planning to ‘Orbánize’ Waste Management

Instead of improving a system based on competition among private entities, MKiŚ is proposing centralizing solutions: producers would be required to pay a fee for placing packaging on the market8, and the National Fund for Environmental Protection and Water Management (NFOŚiGW) would be tasked with overseeing the system and allocating these funds.9 Packaging recovery organizations (OOO) would be dissolved, with NFOŚiGW taking over their role as the sole producer responsibility organization (PRO). Moreover, the fee level would be set by MKiŚ. In practice, this would introduce a command-and-control model of waste management, with all its drawbacks—removing market incentives and increasing bureaucracy.

MKiŚ states in the regulatory impact assessment that the new system is based on the experience of Czechia and Hungary. Czechia is indeed among the EU’s recycling leaders, but the Ministry aims to modify the Czech model by replacing an organization owned by private firms with a monopoly PRO managed by a state legal entity. In 2024, the European Commission indicated that Czech arrangements—under which EKO-KOM is the sole organization authorized to organize the collection and recovery of packaging waste10—may breach EU competition rules.11 The Commission pointed to a conflict of interest, as EKO-KOM is both a market participant and a party to proceedings on the admission of other entities. Czech laws, however, at least allow for the possibility of competition. In Poland, the government plans to create a state monopoly sanctioned by statute.

Hungary has one of the worst systems in the EU: in 2023 only 46.5% of packaging waste was recycled there (compared with 67.4% in Poland). The Hungarian system has been subject to continuous institutional changes that have made it harder for the private sector to operate—both for producers and waste companies. Today, the private sector’s role has largely been reduced to paying a quasi-tax, while recycling rates remain significantly lower.12 13 These solutions are ineffective not only because the tax revenue flows into the state budget, but also because businesses are reduced to mere taxpayers—which does not encourage pro-environmental change.

Moreover, MKiŚ has not presented broader analyses of more market-oriented and decentralized systems operating in countries such as Germany or Belgium, even though expert organizations have recommended looking to such solutions.14 The Belgian system is based on public administration’s trust in businesses, which established the non-profit organization Recupel to manage waste collection.15 Through cooperation with the scientific community, Recupel and businesses introduce innovative solutions that improve waste management. Germany, by contrast, built its model around multiple competing EPR organizations16, which helped increase operational efficiency. When reforming waste management, the government should draw on successful decentralized examples, rather than repeat Hungary’s mistakes.

What About Public Finances?

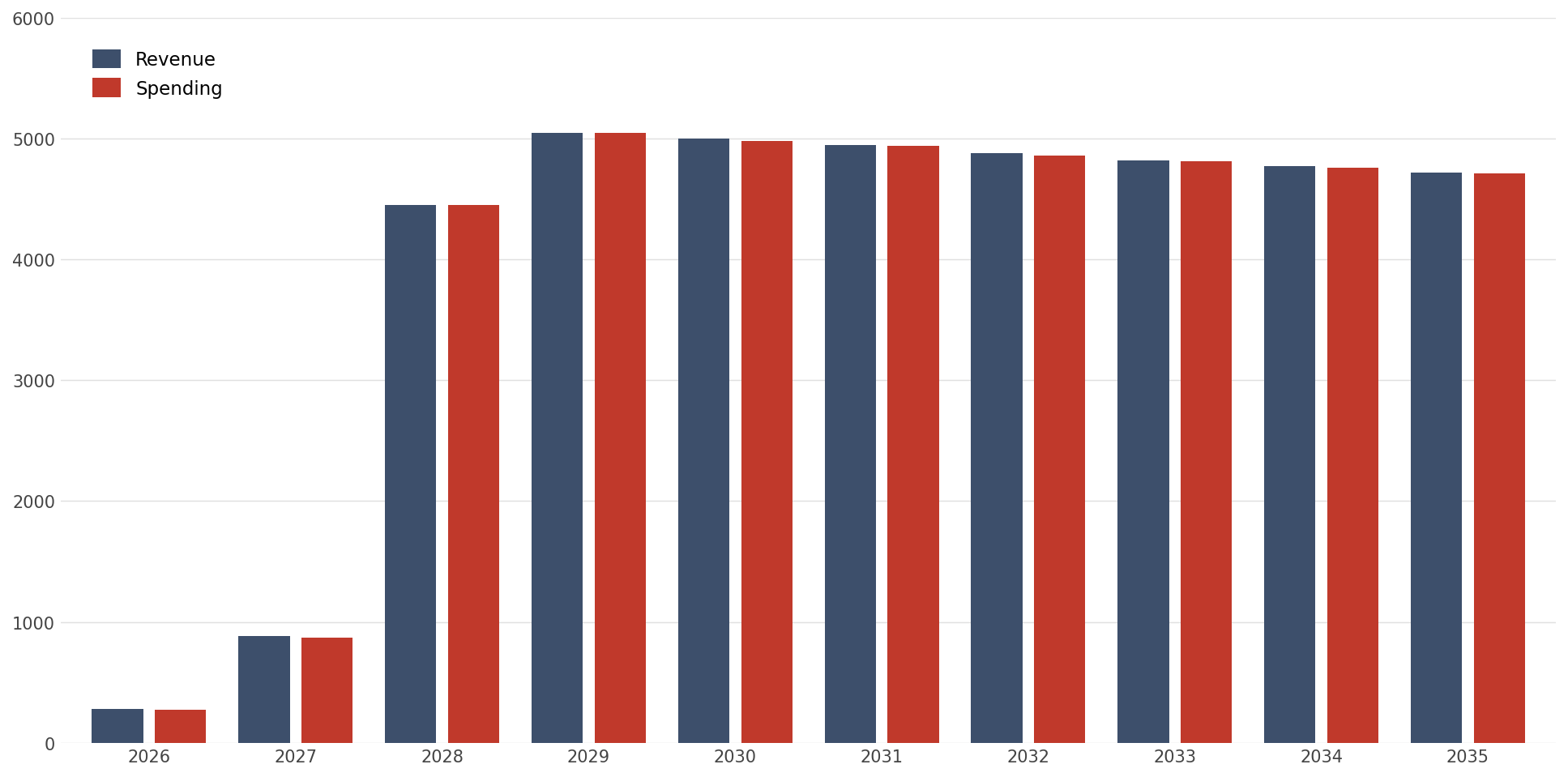

Given the persistently very high public-finance deficit17 (according to IMF projections, the general government deficit will remain above 3% of GDP through 2030), a centralized EPR system could be presented as a way to find new revenue sources for the state.18 In 2028, public-sector revenues from the packaging fee are expected to exceed PLN 4 billion (around 0.1% of GDP). These revenues are to flow to local governments and NFOŚiGW. At the same time, however, the draft act provides that the entire amount will finance new spending. This means that introducing a centralized EPR system will not reduce the public-finance deficit.

It is also worth noting that most of the expenditure will be directed to entities receiving support (around PLN 3 billion in 2028) “to ensure the achievement of EPR targets”. As a result, NFOŚiGW would carry out “a range of processes related to launching and implementing calls, assessing applications and verifying results, concluding agreements, monitoring, controlling beneficiaries, and reporting”. This implies further bureaucracy in waste management. It should also be noted that the collapse of existing packaging recovery organizations may reduce the state’s tax revenues.

A major risk is that the EPR system would be managed by a state legal entity. Practice shows that such entities are often used for purposes other than those originally intended, and they are subject to significantly weaker oversight. In this case, the attempt to avoid a Hungarian-style scenario by directing the fee to NFOŚiGW may create entirely new problems.

Figure 3: Impact of the proposed EPR system on public finances (PLN million)

Source: FOR’s own calculations based on MKiŚ data.

History shows that centrally planned systems in the economy are ineffective. As the Hungarian example illustrates, the same applies to waste management. The changes proposed by MKiŚ will also not improve public finances: new EPR fee revenues will serve to finance new expenditure, rather than reduce the deficit.

Written by Marcin Zieliński – FOR President and Chief Economist & Mateusz Michnik – FOR Economic Analyst